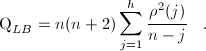

The Ljung-Box test is based on the autocorrelation plot. However, instead of testing randomness at each distinct lag, it tests the "overall" randomness based on a number of lags. For this reason, it is often referred to as a "portmanteau" test. The Ljung-Box test statistics can be defined as follows:

where n is the sample size, rho(j) is the autocorrelation at lag j, and h is the number of lags being tested. Actually we are testing the hypothesis:

- H: The data are random.

- Ha: The data are not random.

The Ljung-Box test is commonly used in ARIMA modeling. Note that it is applied to the residuals of a fitted ARIMA model, not the original series.